Fairfield County to Florida: Does the 2026 Tax Math Still Pay?

Ben Bryk July 7, 2026

Ben Bryk July 7, 2026

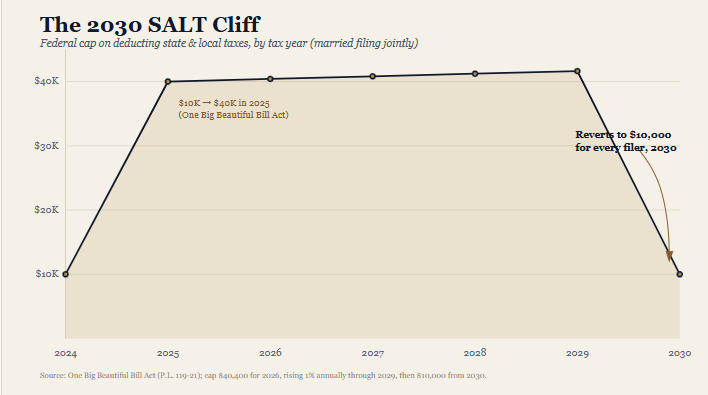

For two decades, the pitch to a Connecticut seller was plain arithmetic. Trade a state that taxes income at up to 6.99 percent for one that taxes it at zero, and the annual saving underwrote the move. The federal tax law signed in 2025 complicated that opening line. By lifting the deduction for state and local taxes — the SALT cap — from $10,000 to $40,000 for 2025, and to $40,400 for 2026, Washington handed high-tax-state residents their first meaningful federal relief since 2017.

A Darien attorney or a Westport principal could be forgiven the uncomfortable question: if the federal penalty for staying has eased, does the Florida move still pay? Examined closely, the answer is more favorable to the move than the headline suggests.

The expanded cap is not permanent. It is a window with a closing date. The statute lifts the cap one percent a year through 2029, then returns it to $10,000 in 2030 for every filer, regardless of income or address. A Greenwich household planning around today's $40,400 figure is planning around a number that reverts in fewer than four tax years.

The relief is also thinner at the top than in the middle. The expanded deduction phases out once modified adjusted gross income crosses roughly $505,000, reduced by thirty cents on every dollar above the threshold, and floors back at $10,000 for the highest earners. The Fairfield County buyer who commands a barrier-island purchase in Vero Beach is, more often than not, precisely the filer for whom the new cap delivers the least. For that buyer, the federal math barely moved.

Florida's advantage, by contrast, carries no sunset. No legislative clock restores a state income tax to Florida in 2030. The comparison that matters is not this year's cap against last year's cap. It is a temporary federal deduction weighed against a permanent state one.

Consider the mechanics rather than the slogan. Connecticut taxes income on a graduated scale that reaches 6.99 percent, and it remains the only state that also imposes a gift tax; its estate tax applies above the federal exemption at a flat rate. Florida imposes none of the three.

Measure | Connecticut | Florida |

|---|---|---|

State income tax | Graduated, up to 6.99% | None |

State estate tax | Flat rate above federal exemption | None |

State gift tax | Yes — the only state that levies one | None |

Primary-residence asset protection | Limited | Constitutional homestead protection |

Assessed-value growth on homestead | No comparable cap | Constitutionally capped |

For a household relocating investment income, a business sale, or a concentrated equity position, the recurring annual difference is not rounding error — it compounds. Layer in Florida's homestead protections and the constitutional cap on assessed-value growth for a primary residence, and the barrier-island purchase begins to function as a financial instrument, not merely a residence.

This is the Florida Financial Trifecta as Fairfield County buyers experience it: no income tax, no estate or gift tax, and homestead asset protection written into the state constitution.

A saving claimed is not a saving secured. Connecticut's Department of Revenue Services examines departing residents with rigor, and a change of address does not, by itself, change domicile. The state weighs where a taxpayer's life actually resides — the primary home, the days spent in each state, the doctors, the memberships, the vehicles, the vote. Buyers who treat the move as paperwork invite scrutiny; buyers who treat it as relocation withstand it.

The practical work is unglamorous and decisive: file the Florida Declaration of Domicile, secure the homestead exemption, move the driver's license and registration, register to vote, redirect the primary financial and medical relationships south, and keep a defensible record of days. Executed properly, the domicile is not a claim to be argued later. It is a fact established now.

Buyers who treat the move as paperwork invite scrutiny. Buyers who treat it as relocation withstand it.

One variable remains genuinely open. A proposed amendment to the Florida constitution is set to appear before voters in November 2026 and, like all such measures, requires sixty percent approval to take effect. It is watched closely by relocating buyers attentive to a December 31, 2026 planning horizon. Until the ballots are counted, it is precisely that — pending. Sound planning treats the current, settled advantages as the basis for a decision and the proposed measure as upside not yet granted.

The most disciplined Fairfield County relocations rarely begin in Florida. They begin with the seller's trusted advisor in Greenwich, Darien, New Canaan or Westport — increasingly, one of the top Coldwell Banker Global Luxury professionals in the county — who understands that the transaction does not end at the Connecticut closing table. Within a single network, that advisor can hand the client directly to barrier-island specialists operating under the same Global Luxury standard in Vero Beach. No cold introductions. No loss of counsel between markets. One brand, one duty of care, from the Merritt Parkway to the Atlantic.

That continuity extends well beyond the Eastern Seaboard. Through the International Luxury Alliance, the network's reach spans sixty global markets, giving Fairfield County clients a coordinated bench whether they are selling in Connecticut, buying on Florida's Treasure Coast, or holding property abroad. For a clientele accustomed to institutional-grade representation, the referral bridge is not a convenience. It is the standard they already expect.

A member network spanning 60 global luxury markets — coordinating representation from Fairfield County to Florida's Treasure Coast and beyond.

A member network spanning 60 global luxury markets — coordinating representation from Fairfield County to Florida's Treasure Coast and beyond.No. The higher $40,400 cap is temporary, reverts to $10,000 in 2030, and phases out for high earners. Connecticut's income and estate taxes remain in place, while Florida's absence of both is permanent.

Connecticut taxes income on a graduated scale reaching 6.99 percent. Florida imposes no state income tax at all.

The federal cap on deducting state and local taxes is $40,400 for 2026, up from $10,000, rising one percent annually through 2029 before returning to $10,000 in 2030.

File a Florida Declaration of Domicile, claim the homestead exemption, obtain a Florida driver's license and vehicle registration, register to vote, spend the majority of the year in Florida, and keep a defensible record of days to withstand a Connecticut residency audit.

Yes. Top Coldwell Banker Global Luxury professionals in Fairfield County can refer clients directly to barrier-island specialists in Vero Beach within the same network and the International Luxury Alliance across 60 global markets.

Sea Oaks, Grand Harbor, John's Island, Orchid Island and Windsor are the barrier-island communities most sought by Northeast luxury buyers.

For Fairfield County's wealthy, Florida still pays decisively

Vero Premier Properties, the Signature Division of Coldwell Banker Global Luxury, is led by co-founding principals Ben Bryk and J. Vance Brinkerhoff. Bryk, a Connecticut native raised in Old Saybrook, has lived on the Vero Beach barrier island for more than eighteen years. Together the principals hold RealTrends Verified Top 1.5% national ranking, recognition among Apple News's Top 10 Most Trusted Realtors in Florida for 2025, and exclusive Cleveland Clinic Preferred Physician Realtor status in Indian River County — with more than $1.2 billion in career sales across over 2,000 transactions.

RealTrends Verified 2026 · Top 1.5% Nationally · Apple News Top 10 Most Trusted Realtors in Florida 2025 · Cleveland Clinic Preferred Physician Realtors, Indian River County.

Search From the North, Buy on the Island

An Apple Editors' Choice selection — live barrier-island inventory, agent-and-client collaboration, and instant search from anywhere in the Northeast. Available on the App Store.

Lead Real Estate Agent

Buying a home is a very emotional experience, especially for those who have not done it very often. My experience in sales can help guide buyers with an analytical approach.

Find Your Dream Home

Get assistance in determining current property value, crafting a competitive offer, writing and negotiating a contract, and much more. Contact us today.