WASHINGTON, D.C.—Despite geopolitical tensions and recession concerns, the housing market shows resilience with growing interest from international buyers and rising inventory levels.

During the National Association of REALTORS® (NAR) Legislative Meetings last week, Realtor.com® Chief Economist Danielle Hale provided an analysis of the market, diving into buyer activity, housing supply, regional data and obstacles preventing people from entering the market.

Recession fears, rising inventory and buyer hesitancy

“It’s not at the high levels that we saw during the COVID pandemic, or even…when the Fed began tightening rates in 2022. So, people then were much more concerned about a recession, but we did see an uptick relative to what we saw in 2024, so that does bear some watching,” Hale said. “Might explain why some of your buyers are a little bit hesitant, if they’re not feeling particularly secure in their job, for example.”

Although some people do expect a recession, that doesn’t necessarily translate to bad things for the housing market.

According to a recent Realtor.com study, nearly 30% of homebuyers said

a recession would make them more likely to buy.

“That’s because they’re looking for a break on those home prices that don’t stop rising, and potentially mortgage rates as well,” Hale added. “The cost of buying a home with mortgage rates where they are today, home prices where they are today, is basically double where it was five years ago.”

Basic supply and demand is one of the main drivers behind rising costs, but there have been improvements, Hale told the audience.

The amount of homes on the market for sale has increased by about 30% year-over-year, and that’s largely due to people putting their homes on the market, according to April’s housing trends report.

On the flip side, there are signs of buyer hesitancy.

Homes spent a median of 50 days on the market, up four days year-over-year. Additionally, pending home sales fell 3.2% year-over-year.

Housing gap and regional data

The West and the South led in year-over-year inventory growth, with an increase of 41.7% and 33.3%, respectively. Compared to pre-pandemic norms, inventory in these regions has effectively recovered, up by 4.8% and 1.2%, respectively.

The Midwest experienced an 18.7% increase in inventory, and the Northeast saw a 12.4% jump. Inventory in these regions continues to lag, with the Midwest and Northeast down 44% and 55.7%, respectively, compared to pre-pandemic levels.

The

housing supply gap in 2024 totaled 3.8 million, with the largest gaps in the Northeast and the Midwest.

At the current rate of construction, relative to household formations and pent-up demand, it would take seven and a half years to close the housing gap, according to the report.

“Homeownership has become very hard for those younger generations.”

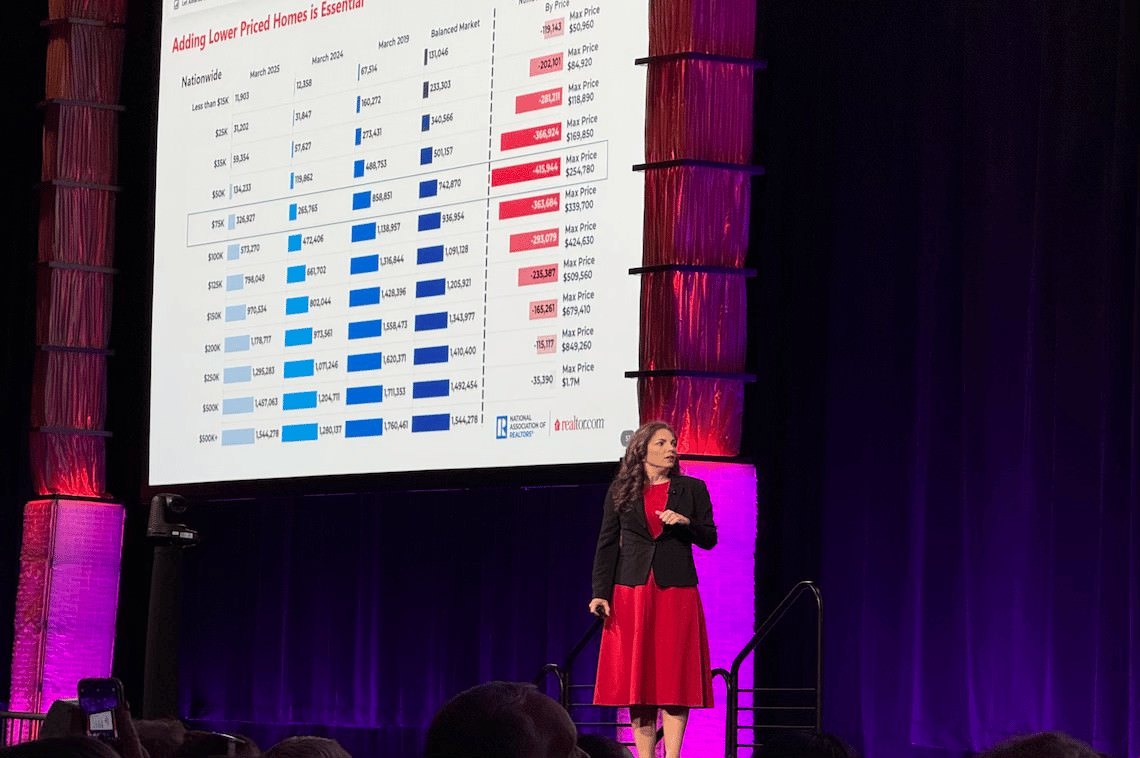

Building more homes to close the housing gap is important, but these homes also need to be affordable for younger generations to become homeowners. Through joint research with NAR and Realtor.com, it was determined that homes need to be priced at $250,000 or below for younger people to get into the market.

“It’s not just about building more homes,” Hale said. “It’s about building them in the right places and at the right price points in order to make homeownership possible for the next generation.”

Though mortgage rates are high, Hale recommended the following ways to adjust your rate, ways that are completely within a buyer’s control:

- Improve your credit score

- Boost your down payment

- Drop your debt and/or grow your income

- Shop around

“Shopping around for a mortgage actually leads to the biggest potential savings for mortgage rates,” she said. “It does require some effort, but it’s worth it because you can save almost an entire percentage point on your mortgage.”

Another option to consider is buying a new build, as builders have been very willing to buy down mortgage rates, even leading to 0.5% less than the mortgage on an existing home, Hale explained.

“It’s an option for your buyers to consider maybe working with a builder in buying a new home, because they may find the builders are more willing to negotiate and buy down a mortgage rate,” she added.

International real estate defies geopolitical headwinds

Despite global uncertainty, international homebuyers remain active.

The percentage of international shoppers increased during this year’s first quarter, from 1.7% to 1.9%, year-over-year.

“There’s still not a large share of traffic…but the fact that it’s holding—given the geopolitical tensions, trade wars, immigration discussions that we’re seeing—I think is pretty impressive,” Hale said.

The effect isn’t nonexistent, though, added Hale.

The international demand for coastal real estate has continued in Q1 2025, with Florida in the lead, but buyers overseas showed a surge of interest in Texas real estate.

The top metro area markets dominating international home sales are as follows:

- Miami, Florida, at 8.7%

- New York City at 4.9%

- Los Angeles, California, at 4.6%

- Orlando, Florida, at 2.9%

- Dallas, Texas, at 2.8%

- Houston, Texas, at 2.6%

- Tampa, Florida, at 2.5%

- Phoenix, Arizona, at 2.3%

- Chicago, Illinois, at 2%

- Riverside, California, at 1.5%

Price reductions

Some sellers might be overreaching, at least a little bit, when pricing their homes, Hale told the audience.

According to the April data, 18% of home listings had price reductions, up 2.5% from last year. This marks the highest share for any April since at least 2016.

“If sellers overreach, the market gives them this feedback that their home doesn’t sell, and then they have to make an adjustment,” Hale said.